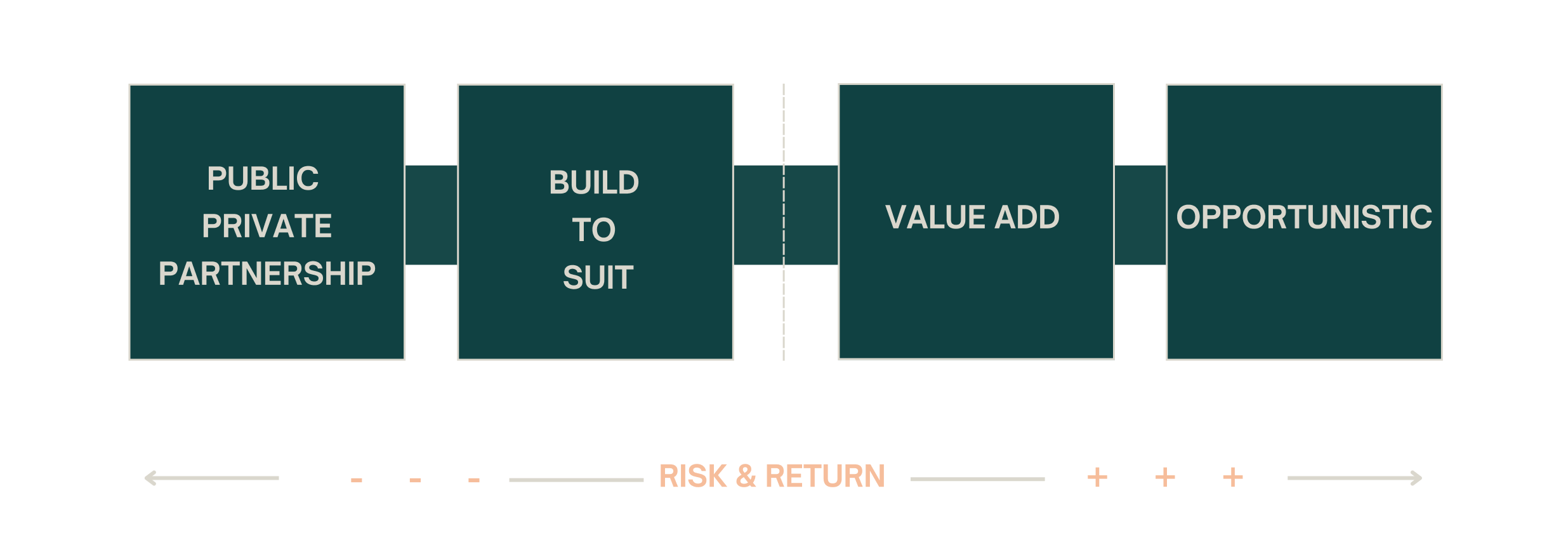

Real estate strategies

In pursuit of the most compelling opportunities, we strategically invest across the risk-return spectrum through the following distinct real estate strategies.

Our (i) public private partnership strategy overlaps with our build to suit strategy, while our (ii) value-add strategy overlaps with our opportunistic strategy.

Our broad investment mandate and opportunity driven approach afford us the flexibility to target and capitalise on the most promising transactions across all four real estate investment strategies.

Public private partnership

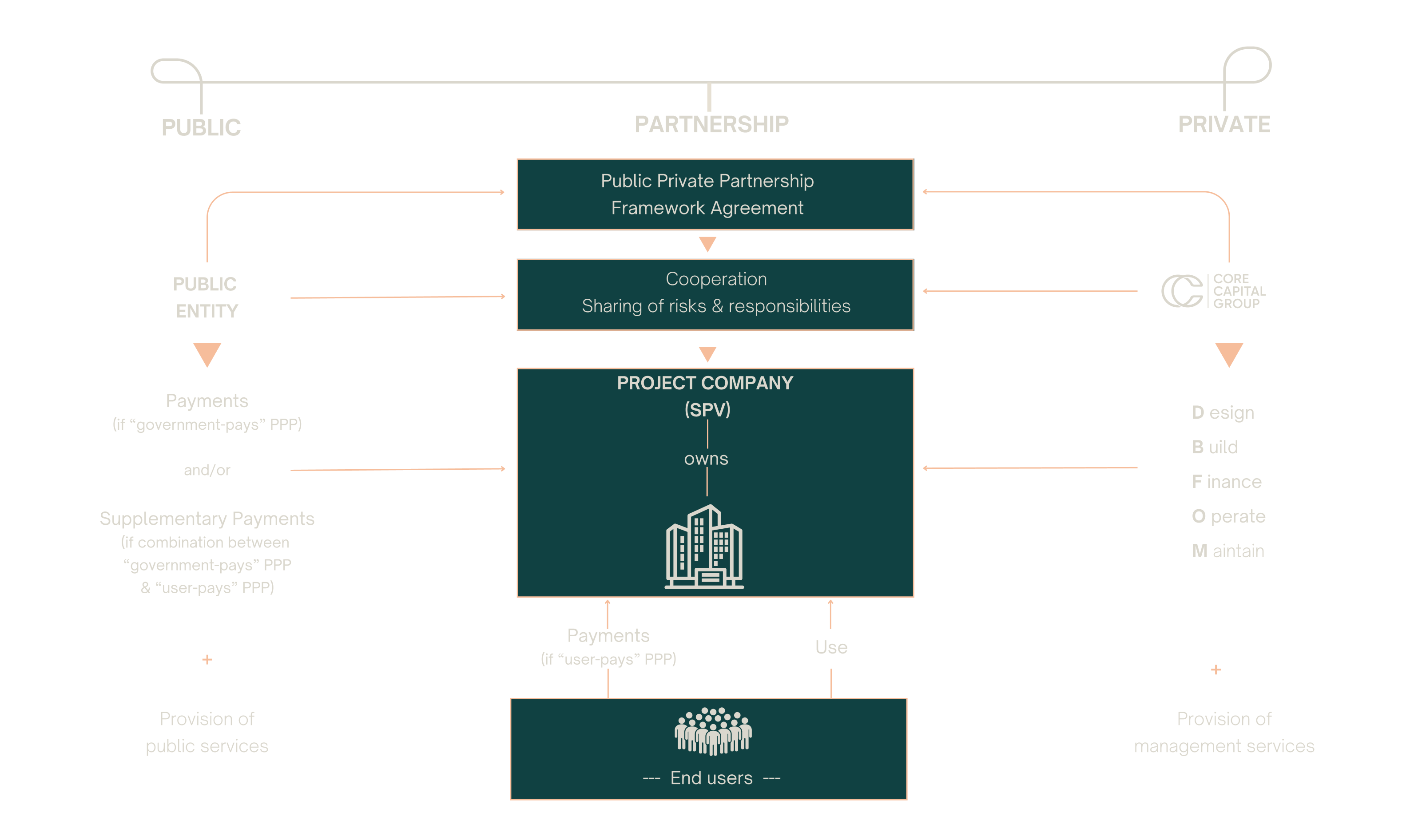

Our public private partnership (PPP) strategy is based on the premise that we (as the ‘private’ party) will work in ‘partnership’ with a government authority (as the ‘public’ party) towards a common goal.

This is achieved by combining the skills and resources of both parties (from the public and private sectors) through sharing of risks and responsibilities in a balanced and structured way.

The starting point is an agreement – between us (as the ‘private’ party) and a government authority (as the ‘public’ party) – to establish a framework for the public private partnership (PPP). In most cases, this framework agreement will cover four key parameters.

%201.png)

Our public private partnership (PPP) strategy typically focuses on greenfield projects (new-build properties) that are intended to be used for housing purposes by specific user groups designated by a government authority.

Each public-private partnership (PPP) is structured to ensure the optimal allocation of risks and responsibilities to the parties best equipped to manage them effectively, with the goal of minimising costs and enhancing performance.

Public sector

The public sector’s contribution will typically be in the form of:

- a contractual obligation to make payments for the use of the property,

- tax incentives,

- the transfer of assets as in-kind contributions (in some cases), and

- other undertakings that support the partnership.

Private sector

Our role will typically involve:

- contributing investment capital,

- applying our expertise in developing, constructing and managing the property, and

- providing additional resources to support the partnership in accordance with the terms and conditions of the public private partnership (PPP) contract.

While there is a wide range of public private partnership (PPP) contract types, we typically use a DBFOM contract, in which the risks and responsibilities for designing, building, financing, operating and maintaining the property are transferred to us.

Design

Designing and developing the property from initial concept through to construction-ready design specifications

Build

Constructing the property and installing all building systems, equipment and fixtures

Finance

Financing the capital expenditure required to design, build and deliver a turnkey property

Operate

Managing the technical operation of the property including the provision of services directly to end users

Maintain

Maintaining the property to a defined standard over the life of the public private partnership (PPP) contract

In select cases, with compelling rationale, we may consider 'user-pays' public-private partnerships (PPPs), where revenue is generated by charging end users – provided that the payments from such users are supplemented by:

- complementary payments from a government authority for housing provided to low-income users, where the rent is capped, or

- subsidies and/or grants from a government authority upon completion of construction or at specific construction milestones.

The public sector benefits from:

- avoidance of upfront capital expenditure,

- efficiencies in construction delivery,

- outsourcing operation and maintenance, and

- improved service levels.

In turn, we benefit by:

- earning a return on our capital investment, and

- generating income through the operation and maintenance of the property.

A public private partnership (PPP) model enables government authorities to:

- attract capital from the private sector – either to supplement public funds or to free up funds for other priority needs,

- improve efficiency – by optimising the use of available public resources, and

- enhance public sector performance and accountability – by reallocating roles, risks, responsibilities and incentives to the parties (in the partnership) that are best suited to manage them.

Active ownership

We are an active, engaged and long-term owner of essential properties that generate stable, predictable, inflation-linked rental income which grows steadily over time and remains resilient across market conditions.

Value-add & opportunistic

Across our value-add and opportunistic strategies, we target undervalued and underperforming properties that have the potential to generate higher cash flows and appreciate in value through the implementation of a clearly defined operating strategy and a well-executed business plan.

Undervalued properties

We target undervalued properties that are typically:

- mispriced relative to intrinsic or replacement value

- distressed

- out of favour or misunderstood by the market

- affected by market dislocation or structural shifts

- temporarily illiquid or capital-constrained

- sold by companies undergoing restructuring of an adverse nature

- acquired through off-market transactions

Underperforming properties

These properties typically underperform due to:

- high vacancy levels

- below-market rental rates

- inflated operating expenses

- inefficient or suboptimal property management practices

- deferred maintenance and physical neglect

- functional or design obsolescence

- reputational challenges affecting tenant demand or investor interest

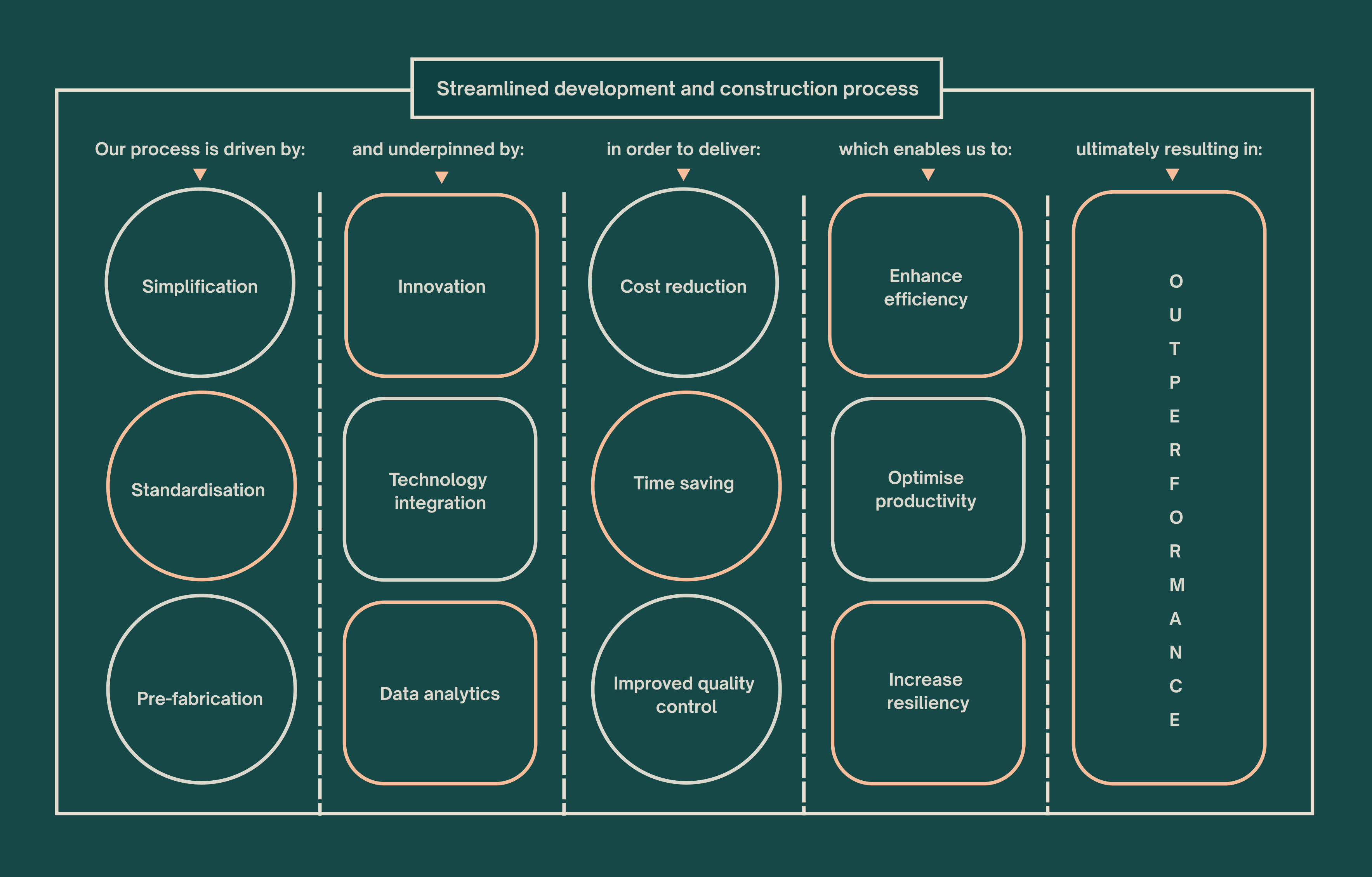

Value creation business plans

By taking a hands-on approach, we strive to create value through:

- new (ground-up) development or redevelopment

- conversion or adaptive reuse

- repositioning or reconfiguration

- renovation or refurbishment

- lease extensions, lease-up strategies and other initiatives to increase rental income

- reducing operating expenses

- implementing consolidation synergies

Common features

The following features are common across all of our real estate investment strategies.

Reclassification from higher risk to lower risk

Our properties are typically classified in the higher-risk category initially, but following the successful implementation and completion of our value creation initiatives, these same properties are likely to be reclassified into the lower risk category as ‘core’ properties.

Transform transitional properties into stabilised properties

Our aim is to:

- accrete value by actively implementing targeted value creation initiatives that minimise the time and cost required to transform transitional properties into income-generating properties, and

- hold the stabilised properties for the long term.

Capitalize on market inefficiencies

The real estate market is inherently inefficient which creates opportunities for those with the insight and rigour to uncover them. We believe that our in-depth knowledge, specialised skill set, extensive experience and relentless effort provide us with a distinct competitive advantage. We use this advantage to prudently invest across our real estate strategies and capitalise on market inefficiencies to achieve superior asymmetric returns

Avoid binary outcomes

Even the most well thought out and well executed plans may produce unpredictable results. To avoid binary outcomes, we prefer to invest in properties that have the potential to gain value through a range of initiatives and benefit from multiple exit strategies. This approach:

- enhances our ability to adapt to inevitable shifts in market dynamics,

- moderates the impact of uncontrollable, adverse fluctuations in the market, and

- provides downside protection

Macroeconomic forecasts & leverage not crucial to our strategies

We do not have (and believe that no one has) the predictive ability required to:

- accurately forecast the future of the economy, interest rates or the broader real estate market, or

- correctly time market movements.

Therefore, we avoid investing in properties whereby value enhancement is solely dependent on favourable movements in interest rates or capitalization rates.

Additionally, we also avoid investments whereby the sole contributor to yield enhancement is the use of leverage.